Italy - The hidden giant in global cosmetics manufacturing and innovation

Italy has a long tradition in cosmetics manufacturing, as well as in botanicals, drug development, machinery and packaging. Combining its strengths in al these sectors together with a renewed interest in R&D, entrepreneurship and business innovation, has led to a quiet yet significant growth of startups and SMEs in Cosmetics and Cosmeceuticals. These are products that sit between cosmetics and pharmaceuticals, using active ingredients and innovative delivery mechanisms - often linked to longevity and regenerative medicine. Both national and regional governments have a strong role to play in supporting this growing industry and attracting investment, especially for early stage startups and innovative SMEs.

SKINCAREBUSINESS INNOVATIONLONGEVITYCOSMECEUTICALSBIOTECHSTARTUPSVC INVESTMENT

Irene Petre

7/1/202610 min read

Italian government has been ramping up efforts to help innovative startups

The government's efforts to stimulate startups across key sectors, including Life Sciences and Technology over the past five years haven't gone unnoticed and the number of innovative start-ups has increased – some of them branching into Cosmetics and Cosmeceuticals, as it is usually much faster and cheaper to bring a product to market than in Pharma and MedTech. There are estimated to be over 820 innovative cosmetics SMEs in Italy (although the definition of what constitutes such a company varies), circa 50% of them with funded growth and circa 31 of them successfully scaling up to series A+ funding rounds. Italy has a long standing brand for botanicals and beauty treatments and deep expertise in manufacturing and chemicals - thus many small entrepreneurs tried to size the opportunity of grants and support in wider Life Sciences and Tech and launch innovative cosmetics and cosmeceutical ventures.

One of the main initiatives the government had taken in collaboration with the private sector was creating CDP VC SGR (Casa Depositi e Prestiti Venture Capital) in 2020 – the main VC operator for innovative startups in Italy, using both public and private funds to help startups(10). The organisation is 100% public but the operating model is based on collaboration and co-investment with the Italian private sector.

Other important VCs in Italy are Angelini Ventures and Indaco Venture Partners – but CDP remains by far the largest source of private investment for early stage startups at national level, acting as a fund of funds – if statistics are correct, in 2025/26 CDP VC has about EUR 4,7bn AUM (with a capital target of EUR 8bn by 2028), whilst Indaco VC e Angelini VC only EUR 350m and EUR 300m respectively (11).

One challenge though in Italy is its geographical fragmentation – there are 21 regions and often each of them run very distinct start-up support schemes, with different levels of venture capital and angel investment. Not all regions have a standalone innovation hub.

Overall, Lombardy is the undisputed engine of the Italian start-up ecosystem, attracting today more than 50-60% of all national VC investments with Life Sciences, Chemicals, Tech and Cosmetics as important sectors. Finlombardia S.p.A. (12) focusses on massive credit-guarantee lines and large scale public – private matching funds to sustain many start-ups and SMEs. Lazio Innova S.p.A. is the regional economic development agency of the Lazio region, which captures roughly 10 – 12% of national startup funding (12), but in terms of Cosmetics startup investment it trails behind Emilia Romagna and Piedmont. Lazio Innova is often considered one of the most proactive, structured and helpful agencies for direct startup support – not necessarily through the largest grants, but they do offer a lot of strategic advice support, business introductions, sponsor travel and events etc.

Emilia Romagna captures around 5 – 8% of national venture capital, concentrated on B2B and Engineering (12). ART-ER, the regional development agency is heavily focussed on operational aspects such as innovation and bridging academic research labs to industry – the region handles financial investment aspects through separate regional entities though. In terms of Cosmetics startups and investment specifically, this region ranks second only to Lombardy and it captures around 11% of Italian cosmetics enterprises.

Apart from these large innovation and startup hubs, there are others emerging such as Veneto and Puglia and of course Piedmont (12) (that is already an industrial catalyst, larger than Emilia Romagna for total startup investment but smaller when it comes specifically to startups in Cosmetics).

Cosmetics in their own remain however a smaller, less essential and thus less supported sector compared to Tech or Life Sciences and innovative Cosmeceutical and Nutraceutical startups often have to piggyback on schemes and grants aimed at Life Sciences, Deep Tech or Agri-food.

Italy is a unique and large cosmetics manufacturing hub in Europe and globally, with a historic tradition in this sector - c. 67% of colour cosmetics and luxury make-up sold in Europe (and 55% of that sold globally) is manufactured in Italy (1). Yet paradoxically it maintains a low profile, meaning it is more focussed on manufacturing and white label, rather than producing strong Italian brands with global recognition and it also assumes a quiet (although growing) position in the innovative anti-aging cosmetics landscape.

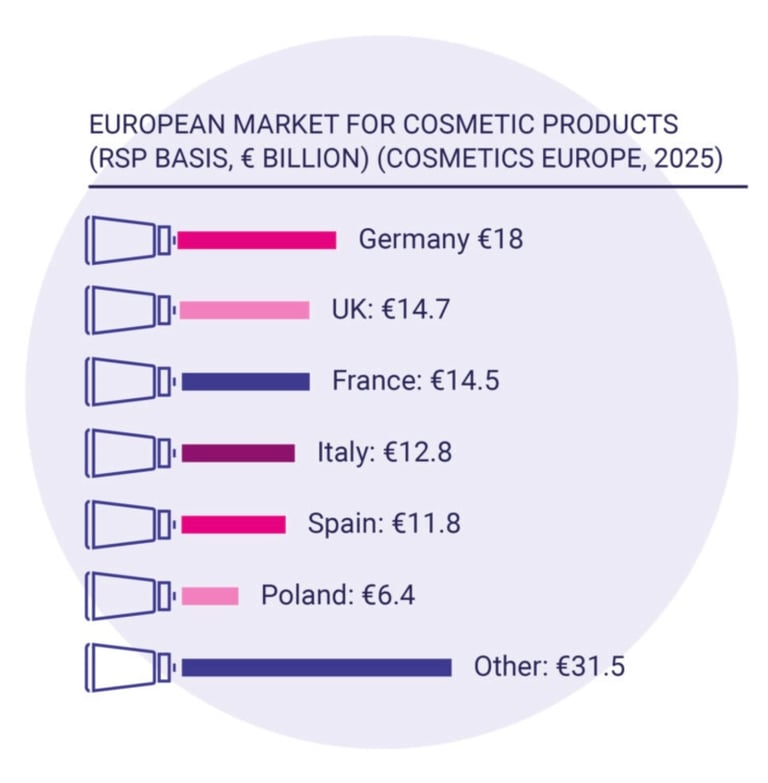

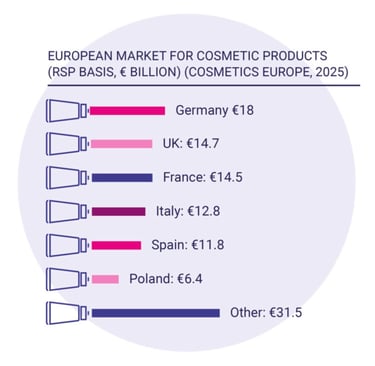

Italian cosmetics industry appears to be the 3rd in Europe (by turnover value, including locally produced cosmetics sold both internally and externally) with an industry revenue of c. EUR 18bn in 2025 - behind France, Germany and ahead of the UK in recent years - and the fifth largest global exporter (with a market share of c. 5,6%) after US, France, Germany and South Korea. Skincare is the largest product category in the European cosmetics and personal care market, accounting for c. 35% of total sales (consumption) in Europe (2).

Although historically Italy has been more representative in the make-up and fragrance areas, in recent years it pivoted towards innovative dermocosmetics and skin longevity (3, 4) – the term cosmeceutical refers to innovative products that sit between cosmetics and pharmaceutical products, in the sense they use innovative compounds and methods to deliver scientifically proven active ingredients to deeper skin levels and influence some biological processes, improving cellular health (5, 6).

Exact numbers of the cosmeceuticals market size in Italy are hard to find, but globally this industry turnover is estimated at around USD 60bn - 70bn in 2025, out of a total global cosmetics market estimated by different sources to around USD 330 - 600bn (7). In terms of cosmeceuticals revenue, skincare products hold the largest revenue share, representing c. 43% of the market, with anti-aging lines leading the charge.

Interestingly, the cosmeceuticals market seems to be driven by Europe, with over 70% of sales in 2024 according to Grand View Research (8) and it seems that European consumers to be much more health and environmentally conscious compared to their American or Asian peers for example - in Europe there is increased demand for vegan and eco-friendly cosmetics and skincare and also for organic and natural ingredients, but with increased efficacy against various dermatological conditions and aging. This is likely to be connected to the fact that white skin is much more prone to visible irritations (9), sun-induced pigmentation or cancer and also to more visible wrinkling.

But still Nessun Profeta in Patria

Italian firms in dermocosmetics lead in advanced structural delivery systems, such as patented stable micelles, microfluidic skin encapsulation or biocompatible vectors. Most of Italian start-ups and SMEs in this sector are focussed on B2B formulation innovation and R&D but very few are successful in B2C, reflecting lower levels of VC funding for early-stage start-ups compared to countries like France and the UK. Being able to play successfully in B2C requires larger marketing budgets, strong distribution partnerships and faster R&D, faster regulatory approvals and market commercialisation - all aspects that require strong investment backing and commercial know-how that angel investors and VCs tend to bring.

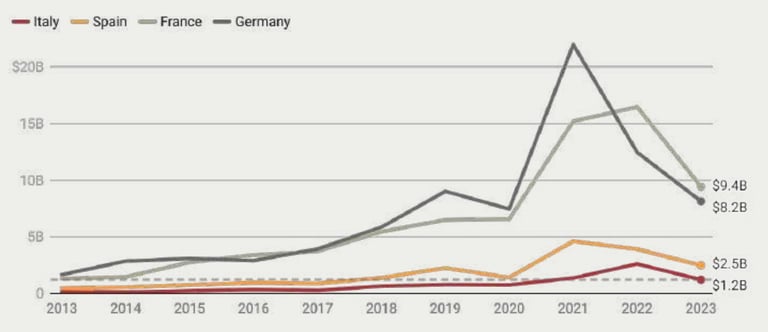

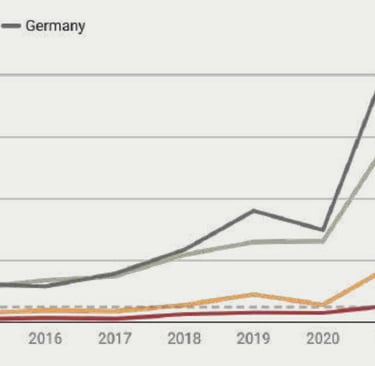

Whilst statistcs about the exact level of private investment in the cosmetics (or skincare in particular) in Italy are hard to find, we found that the Italian Cosmetics sector captured c. EUR 1,8bn of private funding between 2000-2024 from both Private Equity (PE) and Venture Capital funds (VCs) according to AIFI (the Italian Association of Private Equity, Venture Capital and Private Debt) (13) – these funds are however highly concentrated in a number or larger companies and coming typically from slower release mechanisms of PE, rather than VC. As a comparison in more dynamic countries like UK, France or Germany – VC allocations only tend to be around EUR 250m – 350m annually in the UK (so that would be c. EUR 6 – 8bn over the 24 year period in the UK) and around EUR 180m – 240m annually in France (so c. EUR 4,3 – 5,8bn over the 24 year period in France).

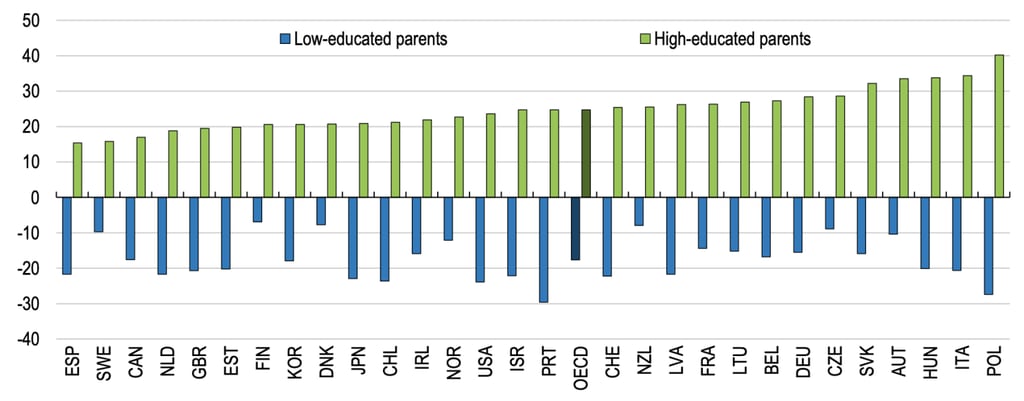

This incongruence between what seems to be a fast-paced level of innovation but very low investment and support, especially in the Cosmetics industry, may seem baffling to the outside world. However Italians understand the phenomenon and have a saying that sums it up: “Nessun Profeta in Patria” (No one becomes Prophet in their own country), meaning it is difficult for people in Italy to re-write their personal history, be recognised as “stars” in one field or another by their own - often tightly knit - communities and thus build credibility and support for anything that seems out of ordinary or too ambitious. Often gifted Italians become “prophets” outside their own country – in places more eager to embrace innovation and people with diverse backgrounds and “strange ideas”. In Italy overall there is pessimism about one’s prospects for work and business success due to complex bureaucracies in almost any sector and due to a “blocked social elevator” – in fact Italy has one of the lowest rates of social mobility in Western Europe (14, 15). A family's socioeconomic status and network of connections in Italy heavily determines their children's ultimate wealth, work and career prospects —far more than in neighbouring European nations (15) and there is a strong inequality of opportunity (16).

For startups this matters a lot, especially in the early stages when entrepreneurs in Italy tend to rely heavily on both moral and financial support from close friends, family and the community. There is academic research directly tracking the impact of family-and-friends backing (“informal finance”) in Italy, which highlights its unique scale. A study from the Einaudi Institute for Economics and Finance (EIEF) utilised Italian census data to track extended family linkages in startup financing (17) and found that Informal finance (relying on family and friends) is highly prevalent in the early stages of Italian business formation, but it statistically reduces the probability of securing professional venture capital later on by 15% to 19% (17). That is because sub-professional networks introduce conflicts of interest and a lack of market validation, which scares off institutional investors. Italian venture capital is overwhelmingly domestic, which naturally restricts funding opportunities to highly localized and personal network (18 ). Data indicates that 71% of all venture capital in Italy comes from domestic investors (19) . For comparison, northern European hubs feature highly internationalised syndicates. Because the pool of Italian asset managers is small—only about 39 to 45 active managers compared to an average of 150 in peer European nations—the ecosystem naturally becomes a "small world" .

Although Italian citizens hold significant private wealth, the institutional venture capital invested is relatively low - both in Cosmetics and in other sectors. That is because Italian investors are more risk averse than their main European peers and check for obstacles in their startup evaluations (20), while also looking for “current social proof” and current product traction, rather than focussing on future potential forecasting and evaluations. This is a lose-lose mentality when it comes to high potential early-stage Italian startups, especially in Life Sciences or innovative cosmetics where R&D, clinical trials and market commercialisation require more time and costs. Also large volume sales do not happen quickly in these cases or do not happen at all without significant injections of capital early on.

The Italian Beauty Valley is expanding – surely but without noise

North of Italy has long standing cosmetic manufacturing hubs in Lombardy and more recently in Emilia Romagna, notably around Bologna - firms have developed a complex ecosystem of suppliers of raw materials, testing, packaging as well as distribution partners and R&D experts, often linked to Academia and various research labs. These dense ecosystem structures have become a competitive advantage for Italy that also allows it to produce quality and innovative products at lower costs compared to players in countries like France,UK, US, Japan or South Korea.

The cosmetics industry is talking about a "Beauty Valley" around Lombardy, including areas like Milan, Crema, Brianza, Bergamo, extending into Lodi and Varese (21, 22) with a high density of CMO (contract manufacturing organisations), especially in make-up and skincare and raw chemical and pharma materials. More recently Emilia-Romagna is establishing itself as well with many cosmetic machinery and packaging firms around Bologna (22).

Historically, CDMOs (contract development and manufacturing organisations) in Pharma and Cosmetics have been seen as non-strategic, bulk production units of parts of white-label products (22). However Italian CDMOs such as Intercos and Ancorotti Cosmetics in Italy are increasingly positioning themselves as strategic partners to larger international players, offering a full-service centred on business, service and product innovation, moving from operational bulk suppliers to innovation partners.

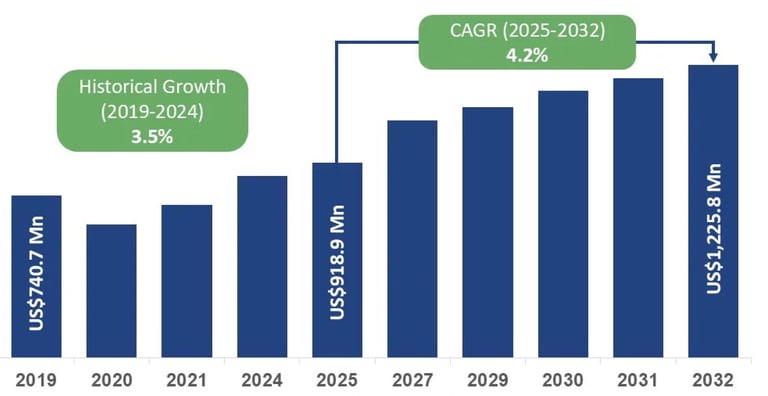

More than half of Italian cosmetic production now comes from CDMOs (Contract Development and Manufacturing Organisations) and according to some sources that can be as high as 65% in 2025 and will continue to grow in coming years (23).

On the other hand, innovative start-ups are developing new branded products with a mix of natural botanical ingredients (in which Italy has a long tradition) with biological active ingredients and innovative technologies, often patented in Italy and internationally. Many products are vegan, halal and eco-friendly - catering to a growing segment of younger educated consumers, often with international profiles, ranging from the US (Italy's number one export country) to the Middle East and more recently China.

However as cosmetic firms, suppliers and distributors in countries like China or India have been developing increasingly localised strategies and business models adapted to their emerging economic, social and regulatory environments post-pandemic – start-ups in Europe need to pay particular attentions when considering such collaborations and perform extensive due diligence on the economic, business, technological and legislative context of such partners as they may be used to very different ways of doing business compared to Europe.

Also developing a more diverse and sophisticated base of angel investors and VCs in the country, able to recognise, understand and properly support “early prophets” in their local communities and overall country, could offer real benefits to the Italian economy, helping business and economic growth and boosting international competitiveness of Italian startups.

Italian CDMO Market Value in Cosmetics, 2019 - 2032f (USD Mn)

European Cosmetics Market - Consumption Value by Country (EUR bn)

c. EUR 8bn of the EUR 12,8 bn Italian cosmetics demand market is represented by consumption of locally produced cosmetics

Italian VC Investments and Number of Start-ups by Area (Cumulative Value by Area, 2019 - 2023, USDm)

Italian VC Investments and Number of Start-ups by Area (Cumulative Value by Area, 2019 - 2023, USDm)

Source: P101 Ventures, Dealroom Data, Registro Imprese

Source: Cosmetics Europe 2025 Data

Source: CEPR EU 2026, OECD Labour Force Statistics 2023

Source: P101 Ventures, Dealroom Data

VC Investments by Key Countries, 2013 - 2023 (USD bn)

Source: Persistence Market Research

Some sources:

https://www.theaestheticedit.com.au/blogs/news/cosmetic-vs-cosmeceutical

https://www.grandviewresearch.com/industry-analysis/cosmeceutical-market

https://www.sciencedirect.com/science/article/pii/S0965206X25000191

https://www.aifi.it/visualizzaallegatonews.aspx?chiave=v7nxSo706r4esD3qH63l8s658vh6e2

https://www.startupbusiness.it/en/startups-and-investments-italy-at-three-speeds/148247/

https://www.sciencedirect.com/science/article/pii/S0276562425000964

https://cepr.org/voxeu/columns/how-far-apple-falls-evidence-social-mobility-across-oecd-countries

interviews with industry figures

https://www.persistencemarketresearch.com/market-research/italy-cosmetic-cdmo-market.asp

*

Here are some examples and case-studies of innovative Italian startups and SMEs in the Cosmetics and Cosmeceutical field:

Case-study 1 - coming soon

IGEA Healthcare

Strategic Advisory for Life Sciences

Switzerland, UK, Italy

contact@igeahealthcare.com

© 2025 - 2026. All rights reserved.