Fewer MedTech start-ups are coming to market in the EU – will the newly revised MDR/IVDR rules shake things up?

Whilst the EU has continued to produce new MedTech startups over the last two - three years, the pace of new companies coming to market has slowed down compared with the pre MDR and COVID years and growth is concentrated in a few large countries with strong funding and regulatory support. The proposed MDR/IVDR revisions announced in December 2025 and AI Act alignment are hoping to reverse this trend from 2026 onwards and instil more agility in the EU MedTech ecosystem.

MEDTECHHEALTHCARE REGULATIONINNOVATION STRATEGYSTARTUPS

Irene Petre

3/5/20266 min read

Whilst the EU has continued to produce new MedTech startups over the past 2–3 years, the pace of new companies coming to market has slowed down compared to the pre‑MDR and COVID years and growth is concentrated in a few large countries with strong funding and regulatory support such as Germany, France, Ireland, Spain, Italy.

SMEs and startups still represent c. 95% of the European MedTech industry, but fewer are reaching late clinical or CE‑marking stages compared with 2018–2020. The bottleneck is not company formation, but market entry and certification.

The EU remains one of the world’s largest MedTech ecosystems with over 30k startups and SMEs, but notes slower company scaling and longer time‑to‑market since MDR/IVDR implementation. There is more focus on Digital Health and AI‑enabled tools, incremental innovation and Platform technologies with staged regulatory strategies. More startups are delaying CE marking or launching first outside the EU in places like Switzerland, the UK and the US.

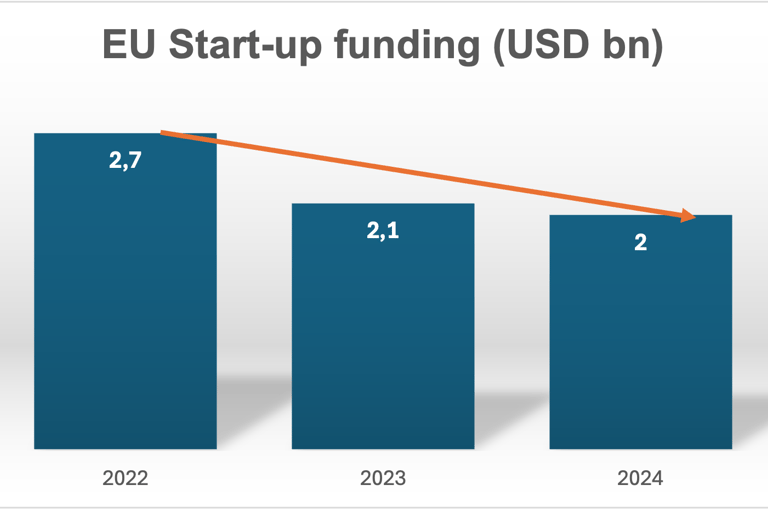

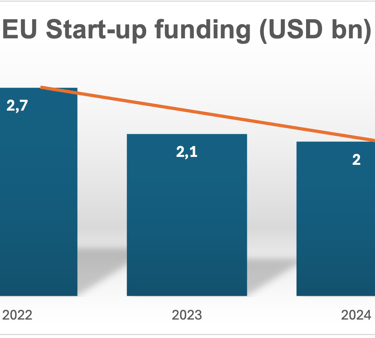

Funding data (which is often the best proxy for startup formation and progression) in the EU shows a slight decline between 2022-24 – which reflects macroeconomic tightening rather than a collapse in innovation but it is of course a factor impacting on the number of startups able to progress to certification:

Several structural factors explain why startup numbers have not accelerated

These factors include:

MDR/IVDR certification costs and timelines disproportionately affect startups compared to larger more established organisations that have more money, expertise and resources to deal with regulation

Notified Body (NB) capacity constraints impact the timelines in which cases can be progressed and certifications issued, delaying market entry for startups

Investor caution around regulatory risk has been on the rise in the last 2 – 3 years

There was a shift towards capital‑efficient digital and AI solutions with stagedregulatory exposure.

The EU Medical Device Regulation (EU MDR) was introduced to improve patient safety standards, strengthen clinical evidence and improve product lifecycle oversight. Yet several years after its implementation, many medtech manufacturers (not just startups but also well established businesses) continue to struggle with the amount of paperwork and (sometimes duplicated) information required, compliance bottlenecks, certification delays, and soaring budgets.

But EU innovation has not declined, only that commercialisation rate has slowed down (fewer startups get to commercialisation), time to reach the market has increased and the process is more selective as only well prepared start-up can get to the finish line in a reasonable amount of time. Others can also make it but with extensive costs and delays.

CAGR -13,9%

Start-ups that succeed tend to initially target lower risk classes and delay CE marking registration

Start-ups that are successful tend to:

Design for lower initial risk classes

Build AI lifecycle, Post-Market Surveillance (PMS) readiness and Post-Market Clinical Follow-up (PMCF) integration early on

Delay full CE marking until product‑market fit is clearer

Set measurable objectives from the beginning

Bring meaningful real-world validated clinical evidence

Have strong alignment with State of the Art processes and cybersecurity

Have clear consistent intended use statements across all channels and materials

Performs a strong benefit - risk analysis

Treat the MDR as a continuous lifecycle obligation – meaning these successful startups see the MDR as a mandatory process that integrates clinical evaluation and real-world data (RWD), risk management, PMS and regulatory planning from product development phases all the way through post-market launch monitoring.

Many EU based startups now incorporate or pilot in the UK or Switzerland and then return to the EU later to obtain the CE marking. That is because UK and Swiss ecosystems currently offer faster regulatory learning, better investor confidence and earlier clinical deployment.

MDR/IVDR revisions are being drafted to cut bureaucracy and costs and help more startups register and commercialise in the EU

The proposed MDR/IVDR revisions and AI Act alignment are expected to improve this picture from 2026 onwards, especially for software‑heavy startups (SaMD).

Some of the key proposed changes that are likely to make a difference for Health Tech start-ups include:

some classification rules are being adjusted and relaxed so that certain device categories will result in lower risk classes, including reusable surgical instruments, accessories to active implantable devices and software

to better distinguish software with life threatening output (so which may directly cause death or irreversible deterioration of health), which likely will remain in higher classes from software with more limited impact (particularly where the digital tool's contribution to clinical decision‑making is indirect or where impact on patient outcomes is limited), These types of SaMD may be down‑classified from class 2a or in some cases from class 2b to class 1 in the future

Two new dispute mechanisms will let manufacturers challenge notified body classifications and permit authorities to reassess CE-marked devices they consider incorrectly classified

notified bodies classifying AI enabled devices will need to demonstrate specific competence in this field (but details have not been published yet) and overall notified bodies are likely to become more specialised than at present

make the MDR certification more affordable, particularly for SMEs and startups - annual monitoring with joint assessment teams is likely to replace the need for recertification every five years, while structured dialogue formalises manufacturer-notified body interaction throughout conformity assessment

representative device sampling, risk-based surveillance intervals and remote audit options are trying to reduce assessment workload for Notified Bodies without compromising independent oversight - thus making the certification process more predictable, affordable, transparent and simple

startups will be able to submit technical documentation, EU declarations of conformity and assessment reports in digital format, making the whole process faster and bringing costs down for startups (new article 52b of the MDR and article 48b of the IVDR)

more product information will be provided digitally, particularly for professional‑use devices (article 110 of the MDR, 103a for the IVDR) and in environments where internet access and electronic documentation systems are reliable. This can allow manufacturers to update safety information more dynamically

having accurate, up-to-date data in Eudamed or linked systems will be increasingly important as authorities may rely more heavily on these systems for market surveillance purposes

for online and digital medtech and diagnostic businesses, the potential convergence of UDI, digital labelling, cyber incident reporting and Eudamed registration suggests that regulatory compliance considerations may extend beyond technical and quality documentation into digital product design and commercial operations

proposed reforms position MDR and IVDR as the primary framework for medical AI, reducing risk of duplicative conformity assessments under the EU AI Act

The AI Act indicates that some notified bodies may be designated to perform conformity assessment for high risk AI systems (article 31 of the AI Act)

the new proposed obligation to report actively exploited vulnerabilities and severe cyber incidents within 30 days to both regulatory and cyber authorities is an important potential change, as it would require significant organisational readiness – start-ups will need to enhance their monitoring and incident management capabilities

For AI SiMD (software AI in medical devices) and IVDs specifically, the Digital Omnibus extends the ultimate compliance deadline to 2 August 2028

EMA (European Medicines Agency) will set up a dedicated support scheme for SME (small and medium size enterprises) device manufacturers, similar to the agency's existing SME support programmes in the pharma field - expected to include guidance on regulatory pathways, classification queries and interaction with notified bodies.

These are not exhaustive - there are other potential changes. Overall, one key takeaway is that the proposed MDR/IVDR revisions introduce targeted clarifications for medical device software (MDSW) and AI‑based devices, especially around classification (Rule 11), lifecycle expectations, PMS, and risk management, and these changes will affect how startups prepare for NB review. The revisions aim to make the framework more proportionate with device risk and innovation‑friendly, but they also raise concerns about reduced scrutiny and inconsistent definitions, which could create uncertainty for early‑stage start-ups.

Feel free to reach out if you would like to know more about this subject or our services.

IGEA Healthcare

Strategic Advisory for Life Sciences

Switzerland, UK, Italy

contact@igeahealthcare.com

© 2025 - 2026. All rights reserved.